Rachel Bowden

Founder & Director

ThinkingAudit Ltd

Introduction

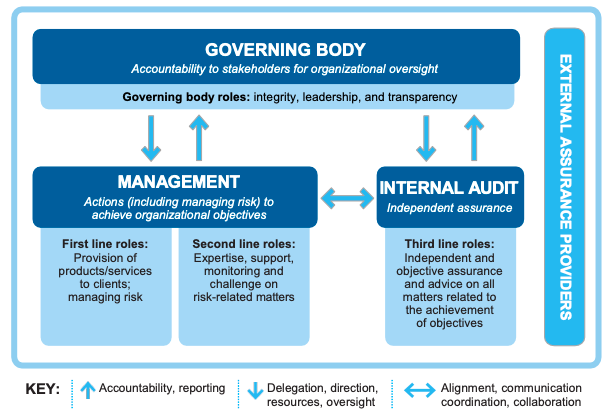

This summer the Global Institute of Internal Auditors published its new Three Lines model, updating the Three Lines of Defence (or Three Lines of Defense for readers on the other side of the Atlantic).

As an internal auditor, I welcome much of the content of the new model, and the steps that have been taken to clarify roles within the framework. However, I worry who else is interested in the model and, if it is just the realm of internal audit, that the model may not gain the recognition of the previous Three Lines of Defence. Additionally many organisations will describe a 'three lines of defence' approach within an assurance framework, risk management framework or approach to governance, but could think harder about what those three lines mean. Certainly I have seen a number of organisations using the Three Lines of Defence model who struggle to clearly describe their second line.

The update should be an opportunity for boards, senior management and their assurance teams to sense-check their current arrangements.

The Three Lines Model shown graphically

© 2020 The Institute of Internal Auditors, Inc.

Key changes

There are a few changes in particular that I think are an excellent change or clarification, and I welcome these.

What I liked less

What next?

It is interesting to read some of the language used, and to compare that with language in the International Professional Practices Framework (IPPF), particularly the Standards. We may be seeing the start of some changes that will filter through to future updates to the IPPF. For example the scope of assurance and advice for internal audit is described in a couple of places as governance and risk management (including internal control).

In conclusion

In writing this, I realise I have seen little mention of the new Three Lines Model anywhere other than from the IIA and internal auditors. The success of the model will be measured by how well it is understood and adopted by organisations, and not just by their internal audit functions. I hope to see audit colleagues and IIA chapters reaching out to colleagues across various professions, and across their businesses to promote and explain the model.

Rachel Bowden

Founder & Director

ThinkingAudit Ltd